THERE were no chartered banks in this country, as the term bank is generally understood, until the Bank of North America commenced business in Philadelphia on January 7, 1782, just eighty days after the surrender of Cornwallis at Yorktown. In 1784, the Bank of New York and the Bank of Massachusetts at Boston opened their doors for business. At the time of the adoption of the Constitution in 1787, these three banks were the only ones in operation in this country. During the next decade more than sixty other banks began operations; at least one in each state along the Eastern seaboard from Maine to South Carolina. In the early days deposits were a minor item in banking operations, the banks being banks of issue, and circulating notes which most banks issued were their chief earning medium.

As banking and trade developed and the notes issued by the many banks found their way into distant communities, need arose for a means of converting such notes into specie or available bank deposits. As a result of this need there grew up in the larger trade centers, exchange and commission brokers who would purchase, in most cases at a discount, notes issued by banks in other cities and towns. The development of this traffic in bank notes led to the publication in the newspapers of bank note lists which indicated the rate of discount at which notes of the outlying banks would be purchased by the brokers in important trading centers.

The notes issued by the early banks did not always possess the desired attribute of universal acceptability. If a Philadelphia merchant, for example, came to New York City with notes of the Bank of North America and tendered them in payment for goods purchased, the dealer in New York might not be willing to accept such notes at their face amount. As a result, merchandise brokers in the important trading centers broadened their activities to include the purchase of uncurrent bank notes, that is, notes that did not circulate freely at their face amount.

Probably the first broker to engage in this business in New York City was Jacob Reed, jun., who had a place of business at No. 10 Burling Slip, foot of John Street. In 1786, when there were but three banks in operation in this entire country, he called attention in a newspaper advertisement to the location of his store, "where every transaction in the Commission and Brokerage business is done with punctuality and precision." He went on further to state, "Cash given for Philadelphia bank notes at a moderate discount." 1

In 1790, Francis White of Philadelphia advertised as a dealer in paper money. He also called attention to the location of his office where, "Will be negociated all kinds of Paper Money and Public Securities, . . . , and such paper money and certificates furnished as will make payment at the Land Office equal to Gold and Silver." 2

In 1791, Manuel Noah, another broker in Philadelphia, advertised that he "Buys and Sells Continental & State Certificates, Pennsylvania and Jersey Paper Money, and all kinds of Securities of the United States, or of any particular State." 3 The "Jersey Paper Money" no doubt referred to colonial notes of New Jersey, as the first bank of New Jersey was not established until 1804.

This type of advertisement continued for many years and several of these brokers broadened their activities to engage in the sale of lottery tickets. Many such places of business later became known as lottery and exchange offices. The operators apparently occupied much the same position in the community that the leading brokers do today, and several of them later combined the sale of lottery tickets with the publication of bank note reporters and counterfeit detectors.

In 1808, Solomon Allen, the son of a missionary preacher on the frontier in New York State and engaged as a printer in Albany, began the sale of lottery tickets to add to his income. In 1815, he and his brother Moses formed a partnership to conduct a lottery and exhange office in New York City. 4 Under the style of S. and M. Allen they conducted their business at 136 Broadway, and in a newspaper advertisement called attention to the "Grand National Lottery for the opening of a canal in the City of Washington." They also advertised that "eastern and southern bills" would be received in payment of lottery tickets at par. 5 In other words, their commission on the sale of such lottery tickets would be partly absorbed by the discount they might have had to take on the conversion or sale of notes which they received. In 1815, B. Jansen, who conducted a lottery and exchange office at 11 Chatham Street, New York City, as an inducement to further the sale of lottery tickets, advertised that bank notes not current in New York City would be exchanged at a moderate premium for lottery tickets. 6 In other words, Jansen was willing to allow a premium on uncurrent notes, thereby partly absorbing his commission on the sale of lottery tickets.

The various forms of paper currency in circulation in the early days of this country were a source of great bewilderment and confusion, not only to foreigners traveling here but to our own citizens as well. Some accounts of contemporary experiences vividly illustrate the confusion that existed.

The experience of a French visitor with Georgia bank notes in 1815 was summarized as follows:

It seems the little man had arrived from Cuba, with about eight thousand dollars in gold, which by way of security he lodged in one of the banks of Savannah.—When he came to demand his money, he was

told that they did not pay specie, and he must therefore take bank notes or nothing. Being an entire stranger, and ignorant

of the depreciation of paper money, arising from the refusal to pay specie, and from the erection of such an infinite number

of petty banks in every obscure village without capital or character, he took the worthless rags and began his Journey northward.

Every step he proceeded his money grew worse and worse, and he was now travelling on to Boston with the full conviction that by the time he got there he should be a beggar.

7

The storekeeper as well as the broker was ever ready to exact a discount on his own part as evidenced by the following early

newspaper account of an attempt to impose upon a laborer:

The traffic of buying up Bank Bills of other states at a discount has become so general, that advantage is taken of it to

impose upon the poor and ignorant, by demanding a discount upon the Bills of Banks in the Northern parts of this state, which

pass as current in this City as our own Bills. An instance of this kind happened no longer ago than yesterday. A poor wood

sawyer received a two dollar note of the [Mohawk] Bank of Schenectady for his labour, and offered it in payment for some necessaries

he had purchased for his family at a grocery and provision store. The storekeeper told him he could not take the bill unless

he would allow him a discount on it. The sawyer thought he earned his money too hard, and had too many children to feed, to

dispose of any part of it in that way, and returning it to the gentleman he took it from, telling him he could not pass it

without giving a large discount, which he could not afford. The Bills of Schenectady Bank are as current as our own, and can

be exchanged for New-York Bank city paper at any moment; a fact which this Grocer must have known. Those who thus attempt

to impose upon the industrious labourer, deserve punishment as much as the man who extorts your purse from you upon the highway.

8

In 1817, only two years after the war of 1812 had been concluded, thirty-nine families in England deputized an English writer

to visit this country to ascertain whether any and what part of the United

States would be suitable for residence. That writer, in the course of his travels in America, visited Cincinnati about November,

1817, and made these observations with respect to the banking and currency situation in that vicinity at that time:

The town contains two chartered banks and one unchartered, all in respectable credit; a branch of "The United States Bank" is also just established there; the paper money system has gone beyond all bounds throughout the Western country. Specie

of the smallest amount is rarely to be seen, and the little which does exist is chiefly cut Spanish dollars, which are divided into bits of 50, 25 and 12½ cents. Notes of 3¼d., 6½d., 13d. and 2s. 2d. are very common;

indeed they constitute an important part of the circulating medium. I purchased Cincinnati notes in Pittsburgh at 5 per cent. discount, and Louisville notes at 7½. This does not proceed from want of faith in those banks, nor are the latter esteemed less safe than the former:

the increase in discount arises from Louisville being 150 miles further distant. The same principle applies to every other town, and operates vice versa upon Pittsburgh. The paper of banks which are not chartered, or which are deficient in reputation, can be bought at similar distances from

the place of its first circulation, at from 10 to 40 per cent. discount: had I sufficiently understood this trade when I landed in America, I think I could have nearly paid my expenses by merely buying in one town the notes of that to which I was going. There

is no difficulty in obtaining them, as there is always a stock on hand at the shavers (brokers) and lottery offices.

9

This same English traveler during his trip of about 5,000 miles in this country, went to a store in Washington to purchase

a pair of worsted gloves which he stated were of the commonest kind and priced at half a dollar. The complications arising

out of this seemingly commonplace transaction were related by him in these words:

I presented a Philadelphia one dollar note; it would not be taken without a discount of 2½ per cent. I then tendered a Baltimore bank [note], of the

same amount. This being one hundred miles nearer was accepted.

The store-keeper had no change; to remedy which, he took a pair of scissors and divided the note between us: I enquired if

the half would pass, and being answered in the affirmative, took it without hesitation, knowing the want of specie throughout

the country, and being previously familiarized with Spanish dollars cut into every variety of size. I now find that demi-notes

are a common circulating medium.

10

The brokers' advertisements previously referred to increased in number and scope as the number of banks increased, and they soon developed into what were commonly known as bank note tables and bank note lists. Such lists were published periodically in most of the newspapers throughout the country and showed merely the names of the banks, their locations, and the discount rate at which their respective notes would be purchased in the larger business centers. Lack of any centralized control over note issues led to wide fluctuations in the quantity as well as the quality of the notes as they circulated and strayed far from the places where they were issued.

In regard to discount rates, the statement was made in 1817 that, "New-York, the great commercial emporium of the United States, may best serve us as the standard place for fixing a value on the different bank notes of our country." The writer of this

continued his remarks as follows:

It is well to observe, however, that the rates of exchange at NewYork, do not fix the real value of the paper (in many cases)

at the places where it belongs; for many banks whose notes are rated at a discount, pay specie as freely as any others—and,

on the whole, the exhibit is rather calculated to shew the course of trade, as to the notes of the good banks, than to give a specific idea of the worth of such; . . . .

11

The publication of bank note tables or lists had not come into very general use prior to 1818, as evidenced by a writer's comments regarding one of these lists that appeared in a Baltimore newspaper.

Niles characterized the business as "shaving of bank notes," went on to state that the table was headed "Course of exchange," and indicated that it "may be useful to some of our readers and deserves preservation as a curiosity." That list contained the names of a few individual banks and the names of several cities in each of about twelve states together with the discount rate at which notes of the various banks in those states would be purchased by the broker who furnished the information. 12

A week later Niles reproduced a bank note table issued by G. and R. Waite of Baltimore which firm also had offices in New York and Philadelphia. He stated that it "may be useful to our distant reader" and concerning the necessity for publishing such a table, worked himself into quite a tantrum, proclaiming: "What a business is this shaving of bank notes! But the misery of it is—that the loss falls upon the productive poor, to pamper the pride and feed the insolence of the dronish rich."

One of the earliest tables and probably the first to appear regularly in a newspaper of general circulation was published every Wednesday and Saturday in The American in New York City. The table which was entitled "Bank Note Exchange," first appeared in that paper on July 14, 1819. 13 It was corrected every Tuesday and Friday by Martin Lee, a Stock and Exchange Broker located at 44 Wall Street.

An example of conditions prevailing throughout the country in these early days is found in the following account of the financial

situation in Ohio. In 1819, Ohio was comparatively a distant point from New York and reliable quotations on the notes of banks located there were not always available. An attempt was made to classify the

banks on the basis of their standing in the community in the following manner:

We have for many weeks past looked in vain in the Ohio papers for

some information respecting the value of the different sorts of bank notes which are sent into this Territory from that state.

A gentleman from Ohio furnished the following information. Seven banks described as Good, five as Decent, four as Middling and four were described

as Good for nothing.

14

The public soon created a demand for frequent and periodic information with respect to the discount rates on uncurrent notes.

A Baltimore publication appears to have been called upon to furnish discount rates, according to the following notice:

At the request of many friends at a distance, we have prepared a list of the prices of bank notes at Baltimore, which shall be corrected and re-published occasionally, or more briefly noticed as the case may require. The price of these

commodities is becoming pretty regular and steady, except as to the bills of bad banks, which should be uniformly rejected, except in

their several neighborhoods, wherein it is presumed that their value must be known.

15

The varying rates of discount on bank notes opened up to the banks the opportunity to buy their own notes at a discount. In Maryland special arrangements were entered into with the note brokers, and it was not unusual for a bank to have agents traveling about for this purpose. After 1818, it became illegal in Maryland for any one to buy, sell or exchange any Maryland bank notes for a sum less than their nominal value, or to employ for the purpose any broker or agent. The law was ineffective and simply added a risk charge to the price asked for such notes. 16

The note brokers, against whom there was an almost continuous fight, were subsequently licensed to operate in Maryland. In 1841, the fight against bill brokers and note shavers was renewed. The cost of their license was raised to $3,000 yearly and the penalty for exchanging and purchasing bills without a license was fixed at $500 for each offense. The banks were released from all obligation to redeem their notes in specie for any foreign or domestic broker. The next year these conditions were mitigated to a considerable extent by a reduction of the license fee to $50. This was brought about by the inconvenience arising from the mass of depreciated and uncurrent paper money, chiefly of banks of other States, which by means of the brokers could be exchanged for reliable currency. 17

The advertisements of the note brokers, together with newspaper announcements of discount rates on paper currency increased in number and scope as the number of banks increased. Bank note tables, beginning about 1820, became a regular feature in newspapers throughout the country, with the information furnished by the brokers and corrected frequently by them.

| 1 |

New-York Packet, August 7, 1786.

|

| 2 | |

| 3 |

Ibid., February 9, 1791.

|

| 4 |

Henrietta M. Larson,

Jay Cooke, Private Banker, 1936, p. 27.

|

| 5 |

New York Evening Post, April 28, 1815.

|

| 6 |

Ibid., August 15, 1815.

|

| 7 | |

| 8 |

New-York Evening Post, October 5, 1815.

|

| 9 | |

| 10 |

Ibid., pp. 287–288.

|

| 11 | |

| 12 |

Niles, August 8, 1818.

|

| 13 |

A table entitled "Bank Note Exchange" was published in the New-York Shipping and Commercial List of July 18, 1817. (See p. 97.)

|

| 14 | |

| 15 |

Niles, September 23, 1820.

|

| 16 |

Alfred Cookman Bryan, "History of State Banking: in Maryland,"

Johns Hopkins University Studies in History and Politics, Ser. XVII, Nos. 1, 2, 3 (1899), p. 68.

|

| 17 |

Ibid., pp. 108–109.

|

THERE are reports of the counterfeiting of paper currency in China as early as the eleventh century, so that it is not surprising

that soon after paper money appeared in this country it was counterfeited. The Bank of England, established in 1694, was not confronted with the counterfeiting of its notes until many years after it commenced business.

The following account of the discovery of the first counterfeit notes by "The Old Lady of Thread-needle Street" presents an

interesting report:

The day on which a forged note was first presented at the Bank of England, forms a memorable era in its history. For sixty-four years the establishment had circulated its paper with freedom; and

during this period no attempt had been made to imitate it. He who takes the initiative in a new line of wrong doing has more

than the simple act to answer for, and to Richard William Vaughan, a Stafford linen-draper, belongs the melancholy celebrity

of having led the van in this new phase of crime, in the year 1758. The records of his life do not show want, beggary, or

starvation urging him but a simple desire to seem greater than he was. By one of the artists employed, and there were several

engaged on different parts of the notes, the discovery was made. The criminal had filled up to the number of twenty, and deposited

them in the hands of a young lady to whom he was attached, as a proof of his wealth. There is no calculating how much longer

Bank notes might have been free from imitation, had this man not shewn with what ease they might be counterfeited. From this

period forged notes became common. The faculty of imitation is so great, that when the expectation of profit is added, there

is little hope of restraining the destitute or the bad man from a career which adds the charm of novelty to the chance of

gain. The publicity given to the fraud, the notoriety of the proceedings, and the execution of the forger, tended to excite

that morbid sympathy which, up to the present day, is evinced for any extraordinary criminal. It is, therefore, possible,

that if Vaughan had not been induced by circumstances

to startle London with his novel crime, the idea of forging Bank notes might have been long delayed, and that some of the strange facts to

be related would never have occurred.

1

While no attempt will be made to review the complete history of counterfeiting in this country, it may be appropriate to present some of the many newspaper and other articles which show how prevalent it was during the State bank note era, and the need for some form of counterfeit detector.

Counterfeiting of paper money in this country began long before the inception of State bank notes. Bradford's New-York Gazette for March 13, 1726, contains this announcement: "Public Notice is hereby given that at Philadelphia they have found out some twelve shilling bills that are counterfeit. They are newly printed and very artfully designed." 2 Shortly thereafter the public was cautioned to beware of "false Jersey money" that was passing in Philadelphia. A detailed description of thirty shilling and three pound bills was given and the following statement was made: "It is supposed these counterfeit bills came to New York in one of the last vessels from England. A large sum is already past there." 3 The Continental currency also came under the evil eyes of the counterfeiters and many interesting accounts of their work on such currency may be found in Historical Sketches of American Paper Currency, Second Series, published by Henry Phillips, Jr., in 1866.

The dissemination of news about counterfeit notes in the early days was mainly through the press, and early newspapers contain many reports of counterfeits and counterfeiting. The Bank of North America in Philadelphia, which began business on January 7, 1782, was, as previously stated, the first bank organized in this country. It no doubt began issuing circulating notes shortly thereafter, as the Pennsylvania Legislature passed an act on March 17, 1782, making it a crime "to alter, forge, or counterfeit any Bank Bill or Bank Note or tender in payment, utter, vend, exchange or barter any such forged, counterfeit or altered Bill or Note of the bank."

The counterfeiters, then as now, lost little time in bringing into circulation imitations of new currency issued by the banks and the government. As a matter of fact, only fifty days after the reduced size currency, now in use, began general circulation on June 10, 1929, a ten dollar counterfeit note of this new series was discovered. As early as 1794 the Bank of the United States and the Bank of North America in a joint announcement cautioned the public to beware of counterfeit five dollar bills of the Bank of the United States and twenty dollar bills of the Bank of North America. The notice describes how the counterfeit notes differ from genuine notes, and indicates among other things that "The Signature of J. Nixon [President of the Bank of North America], has the appearance of being written with lamp-black and oil, . . . ." The notice states further, "It is supposed these forgeries were committed in some of the Southern States, as all the counterfeits that have appeared, have come from thence, and two persons have been apprehended in Virginia, on suspicion of being the authors of them." 4

In 1795, the public was warned to beware of counterfeit bills of the Bank of New York, "one of 40 dollars, and one of 5 dollars, having been detected at the Bank, . ..." 5 In Boston a news item informed the public that a most barefaced species of counterfeit ten dollar bills of the Bank of the United States had been discovered in that city. It went on to state, "the paper is coarse and heavy, without a water mark, Thomas Willing's name is wretchedly imitated, ...." 6

Newspaper publishers in general believed that news of counterfeit notes was of considerable interest to their subscribers as evidenced by the following notice:

We stopped the press to insert a piece of information which must be esteemed eminently important to the Public. It is discovered that the Twenty Dollar Albany Bank Bills, have been counterfeited, and many of them are in circulation. Notice to this effect has been given to the Cashier of the Bank of New York, by the Cashier of the Bank of Albany. Not having received the specific marks that distinguish the counterfeit from the genuine, we can only mention it generally, to induce greater caution. 7

The expansion of the note issues of the banks brought about an expansion of the crime of counterfeiting, which was a source

of great annoyance and considerable monetary loss. The following account of the counterfeiting of notes of the Philadelphia Bank is no doubt indicative of similar conditions in other places at that time:

So serious had this become [the crime of counterfeiting], that in July, 1808, it was determined to change the whole form of

the notes, which previously had been printed in ordinary types, and a committee was appointed to procure types with special

devices for printing the notes thereafter. Bank officers, and particularly the cashier, were repeatedly sent to various places

to testify against counterfeiters who had been arrested. Detectives were paid for hunting the counterfeiters, and a constable

in 1809 was given $15 for making an arrest, while $100 about the same time was contributed "to assist in the arrest" of a

notorious counterfeiter; and the Bank also gave liberally to the constables and to funds for this purpose.

8

Further evidence of the prevalence of counterfeiting in the early days of this country is indicated in the following account:

For many years past the people of the Eastern States have been much vexed and injured by a gang of counterfeiters, chiefly

rendezvousing in

Canada

, and detection was rendered more difficult on account of the impossibility of acquiring a critical knowledge of the numerous

and dif-

ferent notes in circulation. But, latterly counterfeits to a prodigious amount have been discovered on the banks of the middle

states, some of which are admirably executed. If able to obtain a list and description of them, it shall have a place in The Register. It is stated that three persons were taken up at Washington city a few days since, one of whom had in his possession counterfeit

notes to the amount of $62,000.

9

A few years later these comments were made: "Sundry counterfeiters of bank notes have lately found 10 or 15 years honest employment in the penitentiaries of the several states. If their morals be not corrected, they will, at least, be kept out of harm's way." 10 A week later Niles referred to a statement by a judge to a jury that, "A fatal error seems to prevail that a person receiving a counterfeit note has a right to pass it." The judge stated further, "Let the counterfeit note be crossed, so that it may not deceive any other person." 11 The crossing of a note was done by drawing one or two heavy ink lines across the note, usually from each upper corner to the opposite lower corner. When genuine notes were crossed in this manner, it indicated that such notes had been redeemed by the issuing bank.

About two years later Niles stated that:

We can hardly open a newspaper without seemingly hearing a bellowing aloud of "counterfeiters" — "more counterfeiters" — "more forgery," and the like. What a pity it is that society should be so much demoralized, and so villainously cheated, for the benefit

of a few dronish paper-lords — less substantial than "men in buckram?"

12

There was no absence of news items pertaining to counterfeiting as evidenced by the notice: "It is with awful feelings, indeed,

that we publish the terrible list. . . , of counterfeited and spurious bank notes, collected within the last eight or nine

weeks, as we happened to meet with notices of such things in the newspapers."

13

Again on this same subject Niles states: "Counterfeiting goes on prosperously and presents itself in so many forms that it

is exceedingly difficult to guard against it. We can hardly take up a newspaper without seeing some fresh evidence of the

prostration of morals caused by the paper system."

14

Further remarks by Niles on counterfeits were as follows:

From all parts we still hear of gangs of counterfeiters or individuals detected, "too tedious to mention." How much of moral

turpitude has the "paper system" heaped upon us!—fraud is called speculation and counterfeits denominated "pictures"— perjury is excused and forgery considered as evidence of courage! It appears to us quite reasonable to believe that not many less than 10,000 persons —paper

makers, engravers, signers, etc. wholesale dealers and retailers of counterfeit money, are wholly or in part engaged in swindling

the honest people of the United States.

15

The public should be exceedingly cautious in the receipt of bank notes, generally, unless well acquainted with them, just

now. The counterfeiters who have been secretly busy for a long time, have sent a flood of spurious paper abroad, some of which

so nearly represents the genuine bills, that it is exceedingly difficult to detect them.

16

The following probably refers to the "pioneer" counterfeiter of State bank notes in this country: "According to the confession of Thomas Davis, who was lately executed in Alabama for counterfeiting, he had been 38 years [since 1785] engaged in that business, during which time he had made 600,000 to 1,000,000 of dollars." 17

Accounts quite similar to the foregoing continued to appear in the newspapers and other publications during the entire State bank note era. It will be observed that all of them were published before a counterfeit detector, as such, appeared in periodical form.

It was not only with counterfeit notes that the handler of paper

money was concerned; he was also confronted in the ordinary course of business with other forms of bogus notes. It may be

appropriate to describe briefly and illustrate several types of bogus notes that were foisted upon the public during the State

bank note era. A counterfeit note has been described as one that resembles and has been copied from a genuine note. It is usually the same size, shape,

pattern and similar in all respects to a genuine note. A spurious note has been characterized as a peculiar style of counterfeit and has been so termed due to the fact that it has been printed

or engraved from an original plate although it bears no resemblance to a genuine note, except as to the name of the bank and

the signatures of the officers. An altered note is usually one where the name of a reputable bank has been substituted for that of a suspended bank. Genuine notes upon

which the amount has been raised to a higher denomination are generally referred to as raised notes. Further details as to several types of fraudulent notes are found in the following contemporary account:

There are now in circulation nearly four thousand counterfeit or fraudulent bills, descriptions of which are found in most

Bank Note Lists. Of this number, a little over two hundred are engraved imitations of the genuine—and but few can be called

good imitations—the residue being in point of general design entirely unlike the real issues of the banks whose names have

been printed on them. These spurious—more properly altered—bills are generally the notes of broken or exploded banks, which

were originally engraved and printed by bank note engravers for institutions supposed to be regularly organized and solvent;

they consequently compare in point of engraving and general appearance with the issues of good banks. The circulating notes

of many of these broken banks have been obtained after their failure, by dishonest persons, who have made a business of erasing

the title and location of the broken bank, and inserting in its place, either by pasting or reprinting, the title and location

of banks in good credit. The spurious bills thus made have been passed upon the public in large quantities, simply because

the character of the engraving has a genuine appearance, and

because few takers of paper money, comparatively, are familiar with the genuine issues of all banks.

During the past year, the circulation of these spurious notes has increased to an alarming extent, an average of no less than

ten per week having made their appearance.

18

Two examples of the counterfeiter's art, among many others, are briefly described in Day's New-York Bank Note List, Counterfeit Detecter and Price Current for August 16, 1830. The five dollar note of the Paterson Bank (Plate I) is described as "5's letter C dated May 1, 1815," and the two dollar note of the Newark Banking and Insurance Company (Plate II) as "2's letter C. Jan. 9, 1822, pay to S. Nicholas, 19 Condit, President, Beach, Cashier."

It will be noted that the latter mentioned note bears two ink lines crosswise on the face of the note. This was usually done to indicate that the note was counterfeit, although it sometimes indicated that the note had been redeemed by the issuing bank and cancelled in the manner stated. The crossing of a note to indicate that it was a counterfeit is in contrast to the present day practice of imprinting the word "counterfeit" on the face of such a note with a rubber stamp. In the days of the Suffolk Bank and the National Bank of Redemption in Boston, the word "Counterfeit" was branded on the face of such a note by means of a hot iron.

Two notes, which on their faces purport to have been issued by the Bank of New York, present good illustrations of spurious notes (see Plates III-IV). These notes circulated in the 1840's and later, and bear no resemblance to genuine notes of the same denominations issued by that bank. In a contemporary counterfeit detector under the name of this bank and opposite the caption "50s and 100s" may be found the bald statement "Refuse All." This was an intimation to the holders of any notes of these denominations that they should be presented to the bank so that their genuineness might be authenticated. Another counterfeit detector in referring to these same notes states: "There are no genuine fifties with 'fifty' covering the left margin from side to side, and there are no genuine hundreds with a large 'C' on each side of the vignette."

| 18 | |

| 19 |

Should have probably read "D. Nichols."

|

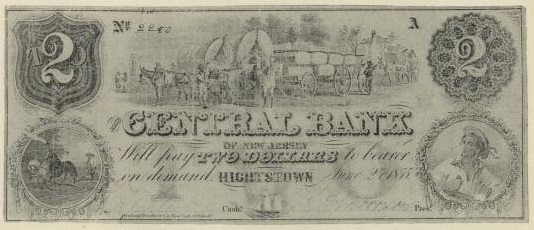

There were many clever operators skilled in the art of altering notes. Excellent examples of their handiwork are found in notes that were originally issues of The Central Bank of Tennessee. There is illustrated (Plate V) a genuine two dollar note of that bank with the main vignette depicting wagons loaded with baled cotton and drawn by oxen and mules. There is also illustrated (Plate VI) a note of the same denomination and of the same bank from which the words "Tennessee," and "Nashville," have been erased and the words "New Jersey," and "Hightstown," respectively over-printed thereon, thus purporting that note to have been an issue of The Central Bank of Hightstown, New Jersey.

It was the practice of these unscrupulous operators to obtain, at little or no cost, notes of banks that had failed and alter them so that they appeared to be the issues of reputable banks. They paid little attention to the relationship of the vignettes to the location of the bank as will be noted from the following descriptions. There are two notes illustrated (Plates VII-VIII), the first of which is a genuine five dollar note of The Central Bank of Tennessee, while the second note was originally the issue of the same bank and altered to The Central Bank of Cherry Valley, New York. That locality was the scene of a terrible Indian massacre in 1778. The main vignette on the five dollar note showing a number of soldiers taking refuge behind a rampart of bales of cotton (The Battle of New Orleans) was in no way connected with the historic background of Cherry Valley.

The Central Bank of Alabama at Montgomery also issued a five dollar note with a vignette showing the Battle of New Orleans, according to an 1857 publication. That publication pointed out in the following manner that notes of The Central Bank of Tennessee had been altered to The Central Bank of Alabama; "5's, Altered from the Central Bank of Tennessee; vig battle of New Orleans; the officers' names, J. A. Fleming, cashier, and H. H. Hubbard, president, are different on the genuine." 20

Another example in the altered category is a two dollar note that purports to be the issue of the Andover Bank, Andover, Massachusetts. Part of the center vignette of this note depicts a cotton plant, at the left end there is a medallion of "Old Hickory" (Andrew Jackson), and in the lower right corner may be found the state arms of Georgia. This note was originally the issue of The Southern Bank of (Bainbridge) Georgia. Other issues of this bank were widely altered.

The practice of altering notes became so widespread that Peterson's Philadelphia Counterfeit Detector and Bank Note List for March 1, 1860, devoted a full page to "Dangerous Alterations." Among the many descriptions of altered notes, the following are typical:

Among the many spurious notes in circulation, there are none that are more calculated to deceive than those printed from the plates of the Waubeek Bank, Nebraska, engraved by Rawdon, Wright, Hatch and Edson, New York, and which are in the finest style.

The plates purporting to have been engraved for this fraudulent [Georgia] concern have been altered to a number of banks throughout the country.

The plates of the Farmers' Bank, Wickford, Rhode Island, have been altered not only to nearly all Farmers' Banks, but also to many other Banks in various parts of the country.

| 20 |

Lord's Detector and Bank Note Vignette Describer (Cincinnati, September 15, 1857.

|

Plates and notes of the broken Commercial Bank of Perth Amboy, New Jersey, are being altered to nearly every Commercial Bank in the United States.

Following each of the foregoing there is a brief description of the various denominations of these bogus notes. It will be observed that in each of these cases, reference has been made to "altered plates." In the first two instances, altered notes of those banks are known to exist.

Brief reference has heretofore been made to altered plates. Notes printed from such plates are less susceptible of detection than in a case where a genuine note has been altered. In the latter instance, when such a note is referred to in bank note reporters, after the description may be found this warning, "hold up to the light." By this means the holder may discern a certain thinness in the paper, particularly under the title of the bank, which in most instances indicates that the note has been altered.

In Petersons' reporter referred to above, under the heading "Union Banks," may be found this warning: "Examine carefully any $5 note having for a vig. a large V., with the heads of five Presidents grouped about it,...." An extremely attractive $5 note of The Union Bank of Kinderhook (New York) dated October 7, 1858, is an excellent specimen of a note printed from the plate described. In this case, the alteration was probably accomplished by hammering out the name of the city or town in which The Union Bank was located and then engraving upon the original plate, "Kinderhook."

Altered notes and notes printed from altered plates were probably the worst hazards confronted by the merchant and the banker

during the State bank note era. What little protection they had was

through the bank note reporters, wherein they would find under various bank names warnings of this type:

20s, altered from the Tenth Ward Bank, New York.

5s, spurious—whaling scene in an arch.

10s, spurious—vig. Neptune and a lady in a car, &c.

5s, altered from Waubeek Bank plate.

500s, from genuine plates, with forged signatures.

20s, vig. ships under sail; unlike the genuine.

In 1819, the Bank of the United States operated a branch, among several other places, at Savannah, Georgia. In February of that year it received from the Planters' and Merchants' Bank of Huntsville, Alabama, in the ordinary course of business and intermixed with other notes, the following notes of the Bank of the State of Georgia; 40 at 100 dollars each and 58 at 50 dollars each. These notes on February 25, 1819, were deposited by the Bank of the United States with the Bank of the State of Georgia with whom it maintained a reciprocal account, their transactions between themselves being almost exclusively in the deposit of their respective notes. About nineteen days later the Bank of the State of Georgia advised the Bank of the United States that the fifty dollar notes had been altered from five dollar notes and the one hundred dollar notes had been altered from ten dollar notes, and asked that they be reimbursed for the excess amount credited to the Bank of the United States.

At that time a total sum of $6,900 was due to the Bank of the United States, which sum included $6,210, the excess amount credited to it by reason of the fact that 98 notes of the Bank of the State

of Georgia had been raised. The Bank of the United States refused to comply with the request of the Bank of the State of Georgia and in order to substantiate the sum due to it, the Bank of the United States found it necessary to bring an action in the Circuit Court of Georgia against the Bank of the State of Georgia. At the trial the Bank of the United States:

... offered evidence to prove, that the officers of the defendants, at the time of receiving the said altered notes, had in

their possession a certain book, called the bank note register of the said Bank of the State of Georgia, wherein were registered, and recorded, the date, number, letter, amount, and payees' name, of all the notes ever issued

by the said bank, by means of which, and by reference whereto, the forgeries or alterations aforesaid could have been promptly

and satisfactorily detected; and further, that so far as related to the said notes purporting to be the notes of 100 dollars,

all the genuine notes of the defendants of that amount in circulation on the said 25th of February, 1819, were marked with

the letter A, whereas twenty-three of the notes of 100 dollars each, so received by the defendants as genuine notes, when

in fact they were altered notes, bore the letters B., C., or D.

21

Further evidence was presented by both sides and judgment was subsequently rendered for the defendants. The cause was brought,

by writ of error, to the Supreme Court of the United States and Mr. Justice Story in 1825 delivered the opinion which reversed the lower court. The full opinion will not be reviewed;

it may be of interest, however, to quote the following pertinent remarks of the Court:

It [Bank of the State of Georgia] is bound to know its own paper, and provide for its payment, and must be presumed to use all reasonable means, by private

marks and otherwise, to secure itself against forgeries and impositions. In point of fact, it is well known, that every bank

is in the habit of using secret marks, and peculiar characters, for this purpose, and of keeping a regular register of all

the notes it issues, so as to guide its own discretion as to its discounts and circulation, and to enable it to detect frauds.

Its own security, not less than that of the public, requires such precautions.

22

A rather crude example of a raised note was that of a one dollar note of The National Bank of Paterson. A genuine one dollar note (Plate IX) of that bank is shown along with another genuine one dollar note of the same bank (Plate X) that has been raised to ten dollars. The workmanship on the raised note is of poor quality. It will be observed that two rosettes in which the figure "10" is centered have been cut from another note or notes and pasted over the "1" at each end of the one dollar note. It will also be noted that a small printed strip of paper reading "Ten Dollars," has been pasted over the words "One Dollar," in the center directly below the title of the bank.

| 21 | |

| 22 |

Ibid., 343.

|

The affairs of the banker in the State bank note era were not only in jeopardy through the prevalence of counterfeit and raised notes; he was confronted at times with a certain amount of risk through the handling of stolen notes. An interesting case pertaining to stolen notes occurred in 1817 as a result of The Salem (Massachusetts) Bank receiving in the ordinary course of business $8,500 in notes of The Gloucester (Massachusetts) Bank and presenting them for payment to The Gloucester Bank about fifteen miles away. The Gloucester Bank paid the notes when presented and about two weeks later discovered that the name of its president had been forged to several of them. Subsequently The Gloucester Bank brought an action against The Salem Bank to recover the amount previously paid and at the trial Cashier Allen of The Gloucester Bank testified that many sheets of their notes had been filled up (numbered and dated) and signed by him and locked up in a desk in the business room of the bank. He testified further that the key to the desk was always kept by himself and that the notes in question had been stolen from the desk by means of false keys in October, 1817, as he supposed, and the name of President Somes had been forged by some person unknown. The notes were dated either July 1st, 1814, or April 25th or May 1st, 1815, and had been signed by the cashier, and not by the president, due to the fact that he seldom went to the bank because of ill health.

The court in rendering its opinion in this case stated that the plaintiffs were not entitled to recover, upon the ground that,

by receiving and paying the notes, the plaintiffs adopted them as their own and were bound to examine them when offered for

payment, and if they neglected to do so within a reasonable time, could not afterwards recover from the defendants a loss

occasioned by their own negligence. In that case, no notice was given of the doubtful character of the notes until fifteen

days after the receipt, and no actual averments of forgery until about fifty days. The notes were in a bundle when received,

which had not been examined by the cashier until after a considerable time had elapsed. The court said further that:

... the true rule is, that the party receiving such notes must examine them as soon as he has opportunity, and return them

immediately. If he does not, he is negligent, and negligence will defeat his right of action. This principle will apply in

all cases where forged notes have been received, but certainly with more strength, when the party receiving them is the one

purporting to be bound to pay. For he knows better than any other whether they are his notes or not; and if he pays them,

or receives them in payment, and continues silent after he has had sufficient opportunity to examine them, he should be considered

as having adopted them as his own.

23

The Court's opinion was summarized in the following words: "Where a banking company paid notes, on which the name of the president had been forged, and neglected for fifteen days to return them, it was held that they had lost their remedy against the person from whom the notes had been received." 24

It will be observed that the Perkins' note, referred to later (Plate XI), bears one of the dates that Cashier Allen testified had been filled in on some of the stolen notes. It does not appear unreasonable to surmise that this very note may have been part of the evidence submitted in this interesting case.

| 23 |

Gloucester Bank v. Salem Bank, 17 Mass. 1 (1820).

|

| 24 |

Ibid.

|

The term broken bank frequently used in bank note reporters, newspapers, and other publications was applied to banks that had suspended operations during the State bank note era, and notes of such banks were commonly referred to as broken bank notes. There has been an erroneous tendency down to the present time to refer to all State bank notes still in existence as broken bank notes. Such a classification does not properly describe all such notes. It is no doubt correct to apply that term to notes of the State banks that failed prior to 1867; it is not correct, however, to apply that term to the solvent banks that had notes outstanding after August 1, 1866. Most of the banks in the latter group complied with the statutory requirements of their respective states, which placed a time limit on the redemption of outstanding notes, and some of those banks will redeem their notes or notes issued by their predecessors when presented today, notwithstanding the fact that in most cases they are not now liable for the redemption of such notes. All such genuine notes might today more properly be collectively known as obsolete notes, a term which includes the notes of broken banks as well as those of reputable banks. The term "obsolete notes" might also be aptly applied to notes still extant of railroads, canal companies, the Confederate States of America, Southern states, and miscellaneous corporations.

Prior to the publication of bank note reporters and counterfeit detectors in periodical form, the dissemination of news of counterfeit notes, as previously stated, was mainly through the newspapers. In the latter part of 1805, the year in which Lewis and Clark com- pleted the first recorded journey ever made across the continent, the number of counterfeit notes in circulation prompted Messrs. Gilbert and Dean, publishers of The Centinel (a newspaper) in Boston, to issue a "sheet" containing a description of counterfeit bills. This is probably the earliest reference to a counterfeit detector and is probably the earliest broadside on this subject. The publishers, a few months later, announced that, "the Public were highly pleased therewith; and doubtless reaped much benefit." The success of the sheet was followed by the publication, under date of June, 1806, of a small twelve page pamphlet entitled, The Only Sure Guide to Bank Bills; or Banks in New-England; with a statement of Bills Counterfeited. Due to the early date of this publication, it seems appropriate to give a somewhat detailed description of its contents.

In the preface to this pamphlet, the proprietors refer to the success of their sheet and state that "as the days increase,

so forgeries also increase; and to keep pace with them, it is found indispensibly necessary to renew the Descriptions, with such alterations, amendments, and additions, as the exigencies of the times demand." The following additional reasons for the publication of this unique pamphlet are

given:

The necessity of having Checks against the inroads of cheats and villains, was never more apparent than of late:—For it very often happens, that the honest

and industrious are robbed of their property and hard earnings, by the imposition of knavery—ignorant

of the method of detecting these Counterfeiters, and their accomplices, the unwary and unsuspecting, are easily taken in; and to add to the aggravation, receive no remuneration for the losses they so sustain!

A sure guide to detect

bank bill

Impositions, is, therefore, a desideratum at the present day;—it is indispensibly necessary.—Such a guide, will be found in the following pages. Messrs. gilbert

anddean, at the urgent solicitation of many friends, and with an industry, perseverance, and correctness, that does them great

credit, have altered, amended and added, considerable, to the late sheet; and their im-

provements, so made, are herewith presented to the Public. If any one should

suffer for want of information, rather than buy a pamphlet, the blame must attach to himself alone; and he will not receive that commisseration which in justice he ought.

Gilbert and Dean announced in this guide that there were 74 banks in the United States, 49 of which were located in the New England States. It contains a list of the New England banks together with the names of the President and Cashier of each bank and the denominations of notes issued by those banks. The denominations of the notes in circulation at that time were in much greater variety than now. The Union Bank of Portsmouth, New Hampshire, for example, issued notes in denominations of 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 15, 20, and 100 dollars. The Norwich (Connecticut) Bank issued among others a 25 dollar bill and the Essex Bank of Salem (Massachusetts) issued notes in the denomination of 30 and 40 dollars.

The guide also contained a brief description of some of the counterfeit notes then in circulation. A counterfeit bill of the Lincoln and Kennebeck Bank of Wiscasset (Maine) was described as follows: "The ten's in the margin, near the vessel on the stocks, have a workshop without windows in the counterfeits; in the true ones the windows are plainly seen; paper whiter and more spungy than the true ones." In the case of the Salem (Massachusetts) Bank, the announcement was made that four and six dollar bills purporting to be the issue of that bank were in circulation bearing the fictitious signatures of the President and Cashier. The further statement was made that the bank had never issued a four dollar bill and that the six dollar bill did not bear any resemblance to the genuine ones.

A New York bank teller in 1853 stated that, "the arts of the counterfeiter have been turned to a comparatively new branch of the profession," known as the alteration of bank bills. That writer was probably not aware of the following statements made by Gilbert and Dean in 1806:

In the case of the Maine Bank, at Portland; "Fifty Dollar Bills, a few in circulation, altered from five dollars." The Nantucket Bank; "Some 2 dollar bills altered to Ten Dollars." The Norwich Bank; "One dollar bills altered to ten—and well done." Twenty dollar bills of the Smithfield Union Bank of Rhode Island were announced as being in circulation, having been, "altered from a one—execution well done, but may be discovered from the word twenty in figures, which are very much crowded together."

The publishers refer to the branch of the Bank of the United States located in Boston and state that the bills of that bank come from the original bank at Philadelphia. They further state that, "Five, ten, twenty and fifty dollar counterfeit bills of the United States bank are in circulation." Following their reference to notes of the Bank of the United States the following statement is made: "All bills in Massachusetts, under five dollars, are of an oval form, and mostly of the [Perkins] Stereotype plate, so that it is impossible to alter them to any other denomination, without immediate detection." Under the reference to notes of the Essex Bank of Salem, this statement is found: "This Bank has recently issued bills from Perkins' beautiful Stereotype." In a notice of two new banks being incorporated in Massachusetts the statement is made that, "Their bills are to be done on Perkins' Stereotype, by order of our Legislature."

In July, 1806, one month after the date shown on their guide, Gilbert and Dean issued a three page postscript containing a description of many new counterfeits that had since come to their attention. In this postscript they made the following statement: "As there appears to be a new gang of villains combined together, who are better workmen than their predecessors, we may expect to hear of more counterfeits until they get routed—and all those which come to our knowledge shall be described as far as in our power, and communicated without delay."

No further results of the labors of Messrs. Gilbert and Dean along these lines have been found and it was some twenty years after the publication of their interesting guide before a counterfeit detector, as such, came into general circulation.

One individual quite conscious of the prevalence of counterfeiting was Jacob Perkins who took a prominent part in the art of banknote plate engraving in the early days of this country. Examples of his work have been referred to previously (Plates XI-XII). He was born July 9, 1766, at Newburyport, Massachusetts, and as a boy was employed by a goldsmith who made dies for copper coinage of that colony. He was a versatile inventor and among many of his creations was a machine for cutting and heading nails in one operation. He designed a plate for a one pound note for the Bank of England. About 1823, he perfected improvements in the steam engine and later established an engineering business, which was carried on by his sons after he died in London on July 30, 1849. 25

Perkins was probably best known for his invention of a stereotype steel plate for engraving bank notes, described by him as having been "made up of fifty-seven case hardened, steel dies, an inch thick, and keyed together in a strong iron frame, which is screwed firm to a metal plate of an inch thickness." 26 It was in this manner that Perkins found means for the important substitution of steel for copper plates in engraving bank notes, thus greatly prolonging the life of the plate. He boasted of the inability of counterfeiters to imitate notes made from his plates. Notes printed from Perkins' stereotype steel plates, however, were counterfeited as have been practically every form of bank note issued since that time. The reverse of a note printed from one of Perkins' Patent Stereotype Steel Plates (Plate XII) shows the care exercised by him in attempting to thwart the nefarious activities of the counterfeiter. While many of the notes printed from plates engraved by Perkins contained various designs and configurations on the reverse, such was not the general practice, as all but a small percentage of the notes then in circulation were issued with the reverse blank. It was not until late in the State bank note era that the general practice was adopted of embellishing the backs of notes with various designs and ornamentations.

One of his observations on the subject of counterfeiting in his early day was as follows: "In the United States, the practice of counterfeiting bank bills has really become a branch of adventurous speculation. Not unfrequently, upon the erection of a new bank, we are presented with counterfeit bills, before we have had opportunity to examine the real." 27

A few months after Perkins' death a writer made the following statement regarding the invention for which he was most famous:

One of the most important of his inventions was in the engraving of bank-bills. Forty years ago counterfeiting was carried on with an audacity and a success which would seem incredible at the present time. The ease with which the clumsy engravings of the bank-bills of that day were imitated, was a temptation to every knave who could scratch copper; and counterfeits flooded the country to the serious detriment of trade. Perkins invented the stereotype check-plate, which no art of counterfeiting could match; and a security was thus given to bank paper which it had never before known. 28

| 25 |

H. P. and M. W. Vowles, "A Study in American Ingenuity and Intrepid Pioneering," Mechanical Engineering, Vol. 53, No. 11, Nov. 1931, pp. 785–790.

|

| 26 |

It is interesting to note the striking resemblance of the practice followed by Perkins in 1806 in the preparation of plates

from which bank notes were printed and the practice now followed by our Bureau of Engraving and Printing. As a matter of fact

the machine now in use, known as a transfer press, represents the evolution and

refinement of the process developed by Perkins. Perkins described this process in the following words:

This principle of making plates combines engraving, etching, and an exact imitation of the most difficult parts of block work,

which has never before been produced. To prevent its being copied with blocks, engraving intersecting with the block work

imitation is added, which gives an impression not within the power of the artist to produce from blocks. To execute this block

work imitation, a long and laborious process is necessary, the expense of which could not be reimbursed, unless a great number

of impressions were wanted. Circular dies, through which is fixed an iron axle, are first prepared, then intersecting lines

are indented, and letters are sunk on their edges; they are then hardened, which contracts the steel; the impression is then

made by these dies on the steel or copper plates, under the pressure of a strong, double jointed, moveable lever, invented

for the purpose, being a new application of that power, the lateral motions of which are produced by fixing a wrench on the

axle of the circular dies, and turning it backwards and forwards, till the cross lines and letters are sufficiently raised.

29

The present procedure in preparing plates from which paper currency is printed is described as follows:

The design is reproduced in soft steel by engravers. Separate portions, such as the portrait, vignette, ornaments and lettering,

are commonly engraved separately by specialists. Each works with a steel tool known as a graver, aided by a powerful magnifying

glass. The finished engraving, known as a die, is heated in cyanide of potassium and dipped in oil or brine to harden it.

The die is then placed on the bed of a transfer press, and, under heavy pressure, a cylinder of soft steel, called a roll,

is rolled over it. The engraving is thus transferred to the roll, in the softer metal of which the lines of the original stand

out in relief. Next the steel of the roll is hardened and the design is transferred to soft steel plates, again by rolling

under great pressure. These plates, with the design in the intaglio or cut-in impression as on the original die, are hardened

and cleaned, and are ready for the printer. The original die

may be used to produce numerous rolls, and each roll is available to make additional plates as those in service become worn.

30

| 27 |

Ibid., p. 3.

|

| 28 | |

| 29 |

Jacob Perkins, op. cit., pp. 5–6

|

Abel Brewster, an engraver located in Philadelphia and a contemporary of Jacob Perkins, published a small pamphlet in 1810 entitled, A Plan for Producing an Uniformity in the Ornamental Part of Bank or other Bills. He indicated that it was useful, "where there is danger of forgery, and for furnishing the public with a convenient and infallible test for the same." He also recommended it "to the careful attention of all who would wish to promote the most effectual means for extinguishing the enormous evil of counterfeiting." In his pamphlet Brewster goes on to describe his plan and discusses a controversy he had with Perkins regarding Perkins' stereotype steel plate. Brewster claimed that Perkins had infringed upon his rights. Although Brewster stated in 1810 that "it is desirable that all Bank Bills in the United States should be uniform, in a considerable part" his suggestion, which might have reduced the amount of counterfeiting, was not adopted until a great many years later.

In 1853, a bank teller of New York City, who chose to remain anonymous, published a treatise on the subject "Bank Note Counterfeits and Alterations: Their Remedy."

His observations and suggestions for the prevention of these impositions have been considered of sufficient interest to warrant

their inclusion in full. They were as follows:

The confidence of the people in the bank note currency of New York has never been so firm as at the present time. This confidence it is for the interest, not only of bank stockholders, but

of the people everywhere, to retain and increase; and under its present general banking law, if its execution is given to

competent, faithful and honest officers, confidence

everywhere in its paper issues will speedily be attained. Presuming, then, that the present law of New York is a good one; that if the securities deposited for circulating notes are received with the close scrutiny the law contemplates,

no loss can hereafter fall upon the holder of its currency; that the millionaire and the poorest laborer alike, whether storing

away at night well filled vaults or a single note, may sleep confident that the morning light will bring with it no news of

sudden calamity or base fraud, by which the accumulations of years, or the hard earned wages of a day, are made but worthless

rags instead of the money they represent; that this law is really worthy of all the confidence it may receive, there still

remains a formidable obstacle to the use of our present paper currency. The difficulty, today, is not so much in obtaining

the confidence of the people in the genuine issues of legalized banking institutions, as in determining which are these genuine issues. When the counterfeiter becomes so skillful that, with his work, he deceives, not only those unacquainted with bank

notes and the usual method of detecting his issues, but good judges; when even bank officers, themselves, receive false issues

with false signatures of their own bank without detection, as in a late instance that came under our observation; when there

are counterfeiters at work in every town, thriving in their lawless occupations, and when each issue of the press announces

a new and still more ingenious result of their workmanship; there would certainly seem to be danger that the whole system

of bank paper for currency may yet have to be abandoned. In such a state of things, not only duty, but imperative necessity

demands of the banker a remedy against so rapidly a growing evil.

Of late the arts of the counterfeiter have been turned to a comparatively new branch of the profession. The counterfeiter,

the educated in his calling, and prince among the rascals of his clique, still finds his trade full of danger and difficulty.

The most ingenious of the race, in many cases, find their work, if not themselves, detected long before a "good circulation"

is obtained. Their work, often prepared with great care and with expensive tools, is frequently detected and announced before

enough is issued to well pay the printer. The part of their trade, therefore, known as the "alteration of bank bills" presents

them with unequalled attractions. With no necessity for tools nor any of the imple-

ments of the old fashioned counterfeiter, requiring only a few easily obtained chemical substances, a fine quality of glue,

and a pair of scissors, to complete their kit, a few hours will transform many an insignificant one to tens and twenties,

apparently as good as ever issued. In these alterations the engraver, instead of being a hindrance, is frequently of decided

service to the counterfeiter. In many instances, using the same die and vignette indiscriminately for the small denomination

of one bank and the large denominations of others, the engraver has already destroyed much of the aid association might furnish

in the detection of altered bills. The counterfeiter, taking advantage of this fact, and clipping, at pleasure, a die or word

from one bill, with little ingenuity can change the denomination of another. To these alterations the notes of all banks are

subject, and no art of the engraver has yet proved a barrier to such tricks. Not only is the prominent die that denotes the

denomination entirely abstracted, and a new one replaced, but even the fine lettering of the border and the centre, with equal

facility are exchanged. If the engraver uses large letters, these disciples of Lucifer either extract the impression entirely,

or themselves use a similar letter for bills not provided with the preventive. Black ink, red ink, large letters, borders

and stripes, although at first of good service, in the end seem to facilitate rather than retard them in the profession they

so perseveringly continue to practice, and the work goes on, filling their pockets, and fleecing many an honest laborer or

tradesman. Yet there seems to be, comparatively, little effort to prevent such transactions. A thorough organization among

bankers, and a fund provided for the purpose of detecting the counterfeiter, an effort to use but one, and that the best,

kind of bank note paper, to increase the variety of engravings so that the same vignette shall not appear upon the issues

of different banks, or at least upon notes of different denominations; to lessen the number and make more uniform the registers'

signatures at the state department; these things, and others that may hereafter be suggested, would do much to make the business

of the counterfeiter more difficult, and to assist in his detection. To prevent the alteration of bank notes a simple remedy

exists, yet untried, and which we have the confidence to believe might, if thoroughly tested, prove a perfect preventive.

The bank teller detects the worst alterations from association, and, if the prominent engraving of a note is

well remembered, he will not be deceived though the pasting process be done with the greatest degree of nicety. If, for instance,

the vignette of some one dollar bill is known to be a blacksmith, the first glance at the engraving will convey to the mind

its value, let the apparent denomination be what it may. If then, the engraver, in making up the plate for a one dollar note, uniformly composes the vignette of one and only one prominent object, the two, three and five, in like manner, always of two, three and five prominent objects; the ten always of more than five, and the twenty of more than ten, no matter what these objects may be, the poorest judge of money cannot be deceived with regard to their value. The fifty,

the hundred, and the thousand dollar note do not circulate so generally, and are always received with more caution, so that

alterations of that kind are comparatively uncommon. In order to make the bank note still more secure, every engraving, whether

large or small, at the end or between the signatures, should also denote the denomination, until to alter a bill will be to

deface its whole appearance. In engraving the different denominations of a bank, the vignette of the one should always be

the smallest in size, the two, three and five gradually increasing, the ten covering one half of the length of the bill, and

the fifty and hundred its whole extent. By this arrangement the engraver may add much to the beauty of a set of engravings,

and need use neither the large red letters nor the heavy border, which so mar the general appearance of the bank note. We

believe that thus, by the help of association, a preventive against all bank note alterations may be obtained, and we hope

yet to see the plan tested by engravers and new banking institutions.

31

Some idea of the prevalence of counterfeiting in New England in 1853 may be gained from the following account:

The whole number of counterfeits, including altered, or notes raised from one to ten, &c., and alterations of bills of broken

to bills of good banks, for New England is eight hundred and eighty-seven; on the banks of Massachusetts, two hundred and eighty; on the banks in Boston, seventy-eight; and on the banks in Providence the large number of one hundred and thirty-eight. Considering the amount and

variety of paper circulated by these banks, that of Massachusetts alone being seven-

teen millions, and the great number of persons engaged in business pursuits, who can have but a limited acquaintance with

it, it is not surprising that the "enemy" should have "sown," in such a "field" of operation, so bountiful a supply of "tares."

32

| 30 |

Facts about United States Money, [U. S.] Treasury Department, January, 1948, p. 5.

|

| 31 |

Mr. John S. Dye, a prominent publisher of books and periodicals, some of which will be described later, gave a lecture in

1856 on counterfeiters and their tricks. The lecture was illustrated by a panoramic display of bank notes on a large scale,

and some of his remarks were reported as follows:

Mr. Dye said, that his object in these lectures was to explain the mode of detecting all classes of bad bills. The idea of

describing counterfeit notes originated with a counterfeiter in Philadelphia, and it has ever since been turned to the advantage of this class of rogues.

There had been a suspicion, he said, that bank-note engravers were the makers of counterfeit money. But this is not so. There

never was but one engraver who turned counterfeiter. The counterfeiters are not so numerous now as formerly. On account of

the great difficulty they have to contend with in the excellent workmanship of genuine bills, they have turned their attention

to making spurious and altered bills. For these they can use one plate for all denominations of bills of every bank in America.

This is done by erasing the title of the bank and names of the state and town, and leaving a blank in the place of the figures

and letters.

The true way to detect a counterfeit is not always by the signatures, but by the workmanship, which is generally coarse and

rough. When a man takes a bill in his hand he should look at every part of it, particularly at the imprint of the engravers.

It is well to look at the letters, to see that they are well formed. Most counterfeits can be detected by the imprint alone.

The panorama now moved, and on canvas, ten by fourteen feet, was exhibited a fac-simile of a genuine five-dollar bill of the

Ocean Bank. Mr. Dye pointed out the beauties of the workmanship of the note, and

said that by the shading of the letters, in ninety-nine cases out of a hundred, a person could tell a good bill from a bad

one. A counterfeit five on the Ocean Bank was also exhibited on the panorama, as the difference could be easily seen, even

by an unpracticed eye.

The lecturer then explained the manner in which counterfeiters make plates and bills. The last new mode is to transfer by

means of white wax. Even by the folds of the dress of the figures on the vignette the work is seen to be imperfect. Counterfeiters

are generally satisfied if they can produce the general features of a bill.

The best counterfeit bill that was ever made was a fifty on the State Bank of Missouri. But it was imperfect in the shading,

and was detected. A counterfeit note is the hardest thing in the world to make, because it must be perfect.

A five-dollar bill on the Farmers' and Mechanics' Bank of Hartford, altered from Pontiac, Michigan, was next shown on the

panorama. It was calculated to deceive all outside of the bank. It was the note of a broken bank, but the plate had been a

good one, and was engraved by Rawdon, Wright & Hatch, of New York.

The next shown on the canvas was a five on the Weybosset Bank, of Providence, Rhode Island. It was a Michigan bill, with the title of a genuine bank inserted. By looking close at the shading around the lettering,

it appeared broken. Everything is complete on the bill, except that the counterfeiter altered it.

The most dangerous of all, a spurious note, was then exhibited. It was a three on the Mercantile Bank, Salem, Mass. Where counterfeiters have got hold of the genuine dies, they might alter that bill to every bank in North America, without altering the title.

The lecturer said that, some years ago, a certain captain got a plate engraved in New York for the Planters' Bank of Alabama. He brought good recommendations, and as it was customary in those days to allow the banks to carry away the plates, the

customer obtained possession of the plate. He went to Lexington, Kentucky, and there joined a gang of counterfeiters. As there was no Planters' Bank of Alabama, they went to St. Louis, had Alabama beaten out of the plate, and Tennessee inserted. It then read "Planters' Bank of Tennessee," and thousands of dollars were made and circulated by the villains.

The panorama next exhibited a fifty on the Providence Bank, Providence, Rhode Island. It is what is termed a raised bill. The bill is genuine in every particular except the denomination, which was altered from

"one to fifty." The counterfeiters probably did this work with a penknife and pen. It is important, to detect this class of

bills, to look close at the letter s in dollars, to see if it has been added.

Another bill represented on the canvas was a twenty on the Manufacturers' Bank, Ware, Mass. It was an altered bill, and the

entire end, where the word "twenty" occurs, had been extracted by a chemical process, and the paper was left almost as white

as it was originally. It can be easily detected by looking at the end piece. This was a one-dollar bill. The "one" has been

scraped off, and "twenty" printed in its place, leaving a whitish appearance around the letters. It can be detected by roughness

all over the face.

In the course of his remarks, Mr. Dye alluded to the great improvements which had been made by bank-note engravers in the

perfection of their work, which now defies the skill of the most ingenious counterfeiters.

33

| 32 |

The general situation with respect to counterfeits, number of banks, and the confused and anomalous condition of the State

bank currency was aptly summarized by a writer in 1864 in lending support of the National Banking System. He said:

In a country like ours, where commerce is the chief pursuit, many social evils are directly attributable to radical faults

in business, which are very easily corrected, and yet are allowed to exist for generations.

For example, counterfeiting is a crime alarmingly on the increase, and one which leads to others of even worse character,

and its very existence is due to the business of the country which tolerates such a system of currency as that with which

we are afflicted.

It is not too much to say openly, and from the results of observation and study, that our paper money, as it now exists, is

an intolerable nuisance, unworthy the genius of a people making as high pretensions as Americans.

In the State of New York are some three hundred banks, with a circulation, in June, 1863, of $32,000,000. Each bank issues notes of the various denominations

from $1 to $500, and very frequently using several plates for engraving the same denomination.